The Portfolio Optimizer for Wealth Management

The Portfolio Optimizer for Wealth Management

With Direct Indexing (DI), instead of buying an ETF that tracks a stock index, we buy the individual stocks. DI can increase after-tax returns through tax loss harvesting (TLH).

DI with TLH intentionally realizes capital losses to offset gains from other sources. The standard industry approach is a simplistic assumption that external gains are unlimited (for long-term) and either unlimited or zero (for short-term). Instead, our system takes in a schedule of expected future gains, allowing clients to see a customized and realistic benefit of using DI.

For more general background on DI, including this scenario's parameters, see here.

All forms of tax loss harvesting, including DI with TLH, increase (on average) after-tax returns by postponing tax payments into the future. This allows the extra funds to grow with the market, even if taxes are eventually paid.

Example: A tech executive is selling stock at her company every quarter as it vests. This is done from an employee share plan, which our software does not control. Assume a best estimate of a long term gain of $10k per quarter, and no other capital losses or gains for the year. To simplify this discussion, ignore:

The client would normally have to pay tax on $40k of capital gains. At a top rate of 20% plus 3.8% net investment income tax, this is $9,520. If we harvest (realize losses) of up to $40k for this year, we can postpone the $9,520 payment. However, if we harvest losses in excess of $40k, we won't get a refund. Instead, we will carry forward any residual losses so that we can use them in future years. Loss carryovers are good to have, all else being equal, because they help reduce future tax liability. However, all else isn't equal here: harvesting a loss will lower the cost basis of the portfolio and increase future tax by an offsetting amount. Although it is still good to capture a loss while it lasts and keep it as a carryover, it is not as valuable.

In general, the benefit of TLH gets smaller as the projected external capital gains go down. Yet, every other implementation of DI with TLH that we are familiar with (as of Nov. 2020) uses a fixed assumption of unlimited external gains, at least for long-term gains. This may overestimate the benefit of DI, but we believe the real reason others use this simplistic assumption is that it is much easier this way. We, on the other hand, always choose sophistication and correctness over ease of implementation. Moreover, our software is purpose-built for tax-efficient investing of separately managed accounts, so we can continue to accumulate such improvements without making it intractably complex.

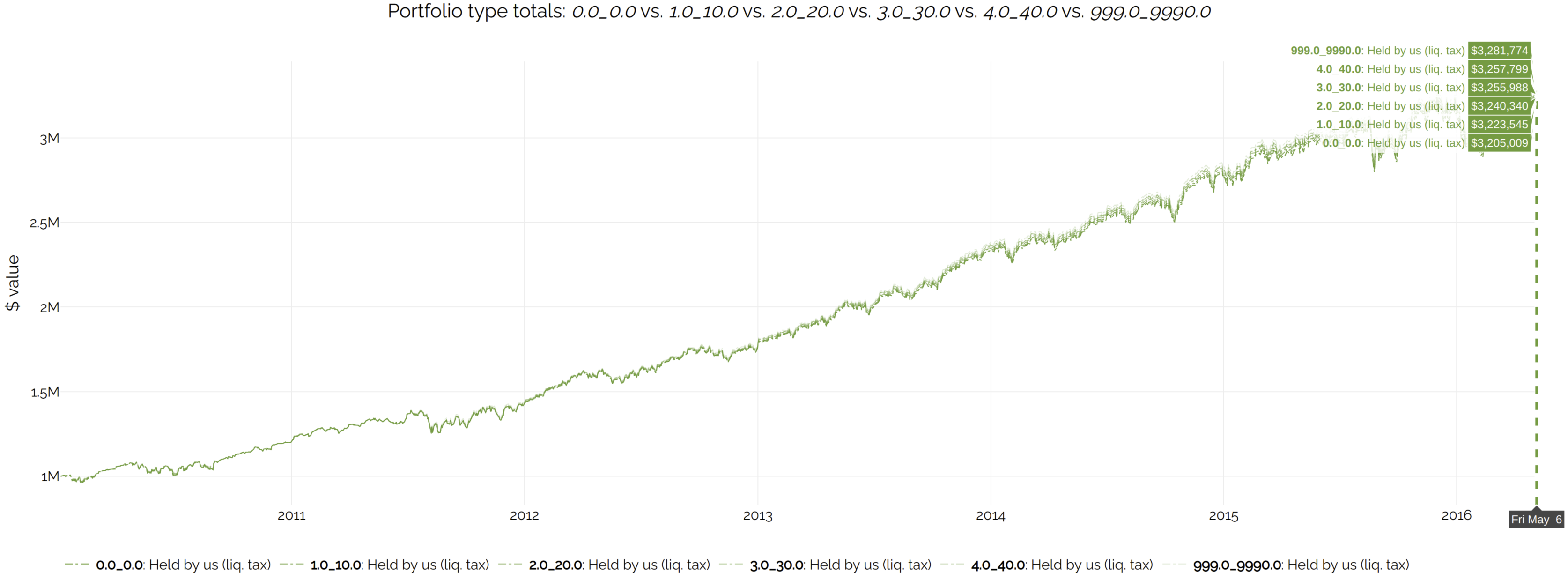

We compare backtests using a liquidation value which includes, for any given day:

Our backtests quantify the increase in after-tax returns of DI with TLH as we increase the assumption of external gains.

The following chart compares scenarios where we expect future annual short-term (ST) and long-term (LT) external gains of $0 ST / $0 LT, $1,000 ST / $10,000 LT, $2,000 ST / $20,000 LT, etc., vs. a baseline of having zero external gains. The line labeled '999' is effectively unlimited external gains - i.e. the most optimistic scenario. Click on this screenshot for an interactive version:

The actual liquidation values are shown below, but the differences are dominated by the scale of the chart. It is a bit easier to see the differences if you zoom in, by clicking on the screenshot to open the live chart, and then dragging a window over an interesting area such as the top-right corner, where the lines start diverging visibly.

Money-weighted returns (not shown in these charts) are the most accurate comparison metric. The improvements in over the 'zero external gains' case are (in increasing order of external net gains) 12, 23, 33, 34, 48 annualized basis points respectively. In the pre-tax case, they are higher (at 25, 47, 71, 75, 89 bps respectively), because this metric ignores the cost imposed by the tax that will be owed eventually. The difference in returns is meaningful, especially as a fraction of the total expected improvement of DI. Note also that the backtest period (2010-2016) was mostly an up market, which makes the differences look smaller.

Our software can generate an accurate estimate of the improvement of DI, which is customized to a client's situation. Using a schedule of expected net gains is better than a one-size-fits-all average, or - even worse - the most optimistic scenario of unlimited external gains when it is not applicable to a client.